BY DEAN BAKER

Photograph Source: John Loo – CC BY 2.0

We got a lot of new data on the economy last week and we will get more this week. Most of what we saw was pretty good from the standpoint of stable growth and slowing inflation, but there is still much ambiguity and serious grounds for concerns about the future.

First, the most important release from last week was the third quarter GDP data. It showed the economy growing at a 2.6 percent annual rate. This is a very healthy rate of growth and follows small declines reported in the prior two quarters.

The growth also should mean that we are again seeing positive productivity growth after seeing a record pace of decline reported in the first half of 2022. Productivity data are always erratic, and the numbers from the first half should not be accepted at face value (reported growth in the fourth quarter of 2021 was an impossibly high 6.3 percent), but there can be little doubt that productivity in the first half of this year was very bad.

The 2.6 percent growth in third quarter GDP was roughly equal to reported growth in hours in the payroll data, but there was sharp fall in the number of people who reported being self-employed. This should imply productivity growth in the neighborhood of 1.0 percent. We will get the actual figure this week when the Bureau of Labor Statistics reports third quarter productivity data.

A 1.0 percent rate of productivity growth is not great, but hugely better than the declines reported in the first half of the year. Productivity was likely weakened in the first half by supply chain problems, huge turnover, and possibly some labor hoarding. These problems should have been less of an issue in the third quarter, and even more so going forward, as the economy is operating closer to normal in most sectors.

Weak productivity would be a major factor raising costs for businesses and thereby creating inflationary pressure in the economy. If we are back on a normal productivity path, this would be a big positive for inflation prospects going forward.

Inflation Data

We also got the release last week of the September data on the Personal Consumption Expenditure Deflator (PCE). This was a mixed picture. The overall PCE rose 0.3 percent, while the core PCE rose 0.5 percent. Both numbers were the same as the August figures, and clearly well above the Federal Reserve Board’s 2.0 percent inflation target.

However, there is some cause for hope that the direction will be downward in the months ahead. First, we know a major factor pushing up current inflation, and especially core inflation is rent. Rent’s weight in the PCE is less than in the CPI, but nonetheless it is a huge factor.

The positive story here is that several private indexes that measure rents on marketed units show rental inflation slowing sharply in recent months. Research from the Bureau Labor Statistics shows that these indexes lead the CPI and PCE by close to a year. This means that we will continue to see rapid increases in rent in the official indices through the rest of this year and into 2023, but can be fairly certain that rental inflation will slow sharply to more normal rates over the course of the year.[1]

We are still seeing a mixed picture in the core goods indexes, with some important items, like vehicles, still showing substantial price increases. However, there is good reason to believe that this will turn around in the not distant future as well.

The price of imported goods has been falling rapidly in recent months. Since April, the index for non-fuel imports has fallen by 2.0 percent. This translates into a 4.7 percent annual rate of decline. By contrast, non-fuel imports prices rose at a 7.2 percent annual rate. Imports are almost 16 percent of our economy, and a much larger share of the goods sector. A huge shift in import prices from rapid increases to rapid declines has to impact the pace of inflation in the goods sector.

This switch will be amplified by the sharp reduction in shipping costs in recent months. After soaring due to supply chain issues last year, shipping costs have declined almost 70 percent from their pandemic peaks. This means that we are likely to see the inflation rate in goods fall sharply in the months ahead and quite likely turn negative.

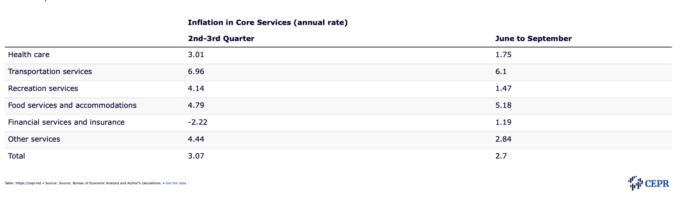

The other big question mark in the course of inflation is non-shelter services. Here too we are likely to see a good picture. Outside of shelter, inflation in core services is relatively moderate and seems to be headed downward.

Here’s the picture.

As can be seen, the inflation rate in these non-shelter core services is relatively modest. The quarter over quarter rate was 3.07 percent. The rate for the last three months was even lower at 2.7 percent. Perhaps more important than the levels here is the direction of change. Inflation in these services seems to be heading lower, not higher, as many inflation hawks have warned.

If we envision a scenario where inflation in non-shelter services remain more or less at its current pace, where the official shelter indexes follow the private indexes for marketed units, and we see low or falling prices for goods, we will be close to the Fed’s 2.0 percent inflation target.

Wage Growth

The most important news on inflation in the next week will be the job growth and wage growth in the October employment report released on Friday. Job growth has been slowing, which was inevitable as the economy approached full employment.

It is likely that job growth will slow further from the 265,000 gain reported for September. The October number is likely to be close to 200,000, which is near a pace that would be sustainable with an economy that is near full employment.

However, the most important number in the October report will be wage growth. There is no plausible story where the economy sustains a high rate of inflation, if wages are only growing at a moderate pace.

We already got some evidence of slowing wage growth in the Employment Cost Index (ECI) for the third quarter that was released last week. That showed private sector compensation increasing at a 4.4 percent annual rate in the third quarter, down from a 6.0 percent annual rate in the second quarter. This pace is still too high to be consistent with the Fed’s 2.0 percent inflation target, but the direction of change is important. The rate of wage growth is clearly slowing even with unemployment rates at very low levels and vacancy rates at historic highs.

The other major wage series that we rely upon is the average hourly earnings (AHE) series, which will be part of Friday’s report. This series differs from the ECI by looking at average wages for all workers. The ECI holds the mix of industry and occupations constant. The change in mix generally does not have much impact, but the two indices have often differed a great deal in the pandemic recession and recovery.

In the downturn, the AHE series showed much more rapid wage gains because many of the lowest paid workers lost their jobs. This raised the average wage by changing the composition of the workforce, even if the pay of people in each occupation and industry did not change. During the recovery this composition effect went the other way, as low-paid workers got their jobs back.

There was also an issue where many workers may have gotten a pay increase by changing their job title. If a worker at a fast food restaurant was promoted to assistant night manager, but their work did not change at all, the associated pay increase would be picked up in the AHE series, but not in the ECI.

Anyhow, the AHE does show evidence of rapidly slowing wage growth. In the last two months, the AHE has grown at just a 0.3 percent rate. This translates into a 3.6 percent rate of annual wage growth. The monthly data are erratic and subject to large revisions, so these numbers must be treated as provisional.

However, if they hold up through the revisions in the October report, and wage growth in the October data is consistent with the prior two months, then we will have pretty solid evidence that wage growth has slowed sharply. In fact, a 3.6 percent annual rate is only slightly higher than the 3.4 percent rate we saw in 2019, when the inflation rate was comfortably under the Fed’s 2.0 percent target.

If the rate of wage growth is in fact 3.6 percent, it is almost impossible to envision a scenario in which inflation remains uncomfortably high. We would need to see a sustained redistribution of income from wages to profits that has never happened before. In short, if wage growth is now near a 3.6 percent annual rate, the Fed has done its job.

Is a Recession Coming?

While the headline GDP growth figure was very positive, many analysts pointed to the fact that it was entirely driven by trade. Rising exports and falling imports added 2.77 percentage points to the quarter’s growth. No one expects that the trade deficit will continue to decline, as a rising dollar makes our goods less competitive internationally. Also, the economies of our trading partners are likely to sink into recession in the next year, due to rising interest rates and the impact of the war in Ukraine. This will seriously dampen demand for our exports.

This means the main source of strength in the third quarter data will not be present in future quarters, however that does not mean the economy’s prospects are entirely negative. First, inventory accumulation, the other major erratic component in GDP, subtracted 0.7 percentage points from the quarter’s growth. We had been seeing extraordinarily rapid inventory accumulation in the prior three quarters, so some drop in the pace of accumulation was not a surprise.

The rate of accumulation in the third quarter was pretty much normal for an economy growing at a moderate pace. Since overall inventory to sales ratios are now close to normal (high in some areas, still very low for vehicles), we may expect comparable rates of accumulation going forward, unless the economy sinks into recession.

The big risk here is the impact of the Fed’s rate hikes. These rate hikes are a major factor in the dollar’s rise, which will be pushing net exports lower. The other area that has been clearly impacted by rate hikes is residential construction. It has fallen at double digit rates the last two quarters and is now 15.1 percent below its peak for the pandemic recovery in the first quarter of 2021.

There are two factors behind this fall. One is the plunge in mortgage refinancing. The fees associated with mortgage issuance are included in residential investment. While purchase mortgages have fallen due to the rise in interest rates, refinancing has virtually stopped after a huge boom in 2020 and 2021. This falloff has been a big factor in the decline in residential investment, but now that refinancing has basically stopped, it can’t fall further.

The other factor is a drop in housing starts. Housing starts are down by almost 20 percent from their peak last year. This will eventually depress construction, but it has not had much impact to date. There is a huge backlog of unfinished houses due to supply chain issues that delayed construction. The number of homes under construction in September was actually higher than at any point in the recovery.

At some point the decline in starts will result in a fall in residential construction, but that will not be in the current quarter, and quite possibly not until the second quarter of 2023. This means that we may see little further decline in residential construction for the next two quarters. The decline in this component in the third quarter subtracted 1.37 percentage points from the quarter’s growth. It is very unlikely residential construction will have a comparable negative impact in the next two quarters.

There is a similar story with investment in non-residential structures. Investment in non-residential structures fell at a 15.3 percent annual rate, subtracting 0.41 percentage points from the third quarter’s growth. Investment in non-residential structures has been falling sharply since the start of the pandemic.

The issue here is that the huge increase in remote work has reduced demand for office space and the increase in online shopping has reduced demand for retail space. While these changes are likely to be permanent, there is a floor as to how far construction will fall.

Investment in non-residential structures is now almost 27.0 percent below its pre-pandemic level. Office construction is down 35.2 percent from its peak, which was in the first quarter of 2020. Construction of shopping centers is down almost 40 percent. And construction of power generation facilities, a very large category in structures, is down almost 43 percent. I’m not sure of the reason for this drop (the plunge began when Trump was still in the White House), but it seems unlikely to continue.

In short, we are likely to see the drag on growth from this sector lesson in the quarters ahead. Even if non-residential construction continues to fall, it is not likely to have anywhere near as large an impact in future quarters.

This leaves consumption and government spending. Consumption grew at a modest 1.4 percent rate in third quarter. A 2.8 percent rise in consumption of services offset a 1.2 percent decline in goods purchases. High interest rates, and reduced home purchases, will dampen demand for vehicles and household appliances and furniture. However, it may not be enough to slow demand much further. This is especially the case with vehicles where a backlog of orders may keep sales up for the next two quarters.

Government spending grew at a 2.4 percent rate in the third quarter. It grew sharply at the peak of the pandemic and then fell back to more normal levels in recent quarters. It presumably will grow at roughly a 2.0 percent rate in the quarters ahead.

In short, there is a real risk of recession, especially if interest rates continue to rise, however it hardly seems like a done deal at this point. Construction, both residential and non-residential, may be less of a drag on growth in the quarters ahead. However, net exports will almost certainly be a large negative. The big risk is that the deterioration in the trade deficit will be so large as to offset positive growth in the domestic economy.

Can the Fed Pause?

The economy is definitely seeing a large impact from the Fed’s rate hikes to date. However, these hikes may not be sufficient to throw it back into recession. If it continues an aggressive path of hikes, then the risk of recession and high unemployment become far more likely.

A large rate hike at the November meeting is all but certain, however if the October employment report again shows a modest pace of wage growth, there will be solid evidence that the Fed has done its job. If the pace of wage growth remains moderate, then the Fed does not need to fear a story of a wage-price spiral, like we saw in the 1970s. In short, the October employment report may provide a very solid basis for the Fed pausing its plans for future rate hikes.

[1] I should note that several economists, most notably Jason Furman, made this point last year in arguing that inflation would rise in 2022. I had thought the rise indicated by the private indexes would be offset by the impact of large-scale evictions when the federal pandemic moratorium ended. The Census Bureau’s Pulse Survey indicated that an extraordinarily high percentage of renters believed they faced an immediate threat of eviction. There was in fact no huge surge in evictions after the moratoriums ended. The gap between the survey and the actual outcome likely reflects a huge skewing in responses in a survey with a response rate near 5.0 percent.